Applying to Med/PA School

5 Ways to Slash the Cost of Medical School

About The Atlantis Team

We offer helpful, informative content to the next generation of healthcare professionals, so that they can achieve their goals, avoid common pitfalls, and grow in their passion for healthcare.

Medical school has a hefty price tag, but are there any ways to make it less expensive? Here are our best tips.

Google Doesn’t Lie

Have you ever begun to type a question into the Google search bar and been thoroughly amused by the results?

Typing in “why” brings up “why do we yawn,” while “why is” results in “why is the sky blue.” Combine “why” and “medical school,” however, and your first hit will likely be the million-dollar question: “why is medical school so expensive?” Clearly, it’s something many students ponder.

Once you’ve read the many articles attempting to explain to you why medical school is as expensive as it is, your next question will likely be: “Okay, so how do I make it cost LESS?” If there is a verifiable way to do that, you’ll want to know about it. And trust us, it’s been done. We have spoken with students who have gotten plenty of scholarship money to put towards medical school, and even one who not only was granted a full ride, but also receives a stipend while in medical school. You read that right, she makes money in medical school.

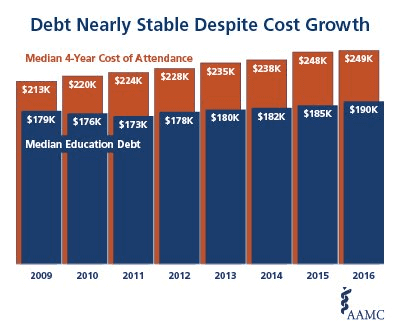

For the average student, however, the cost of becoming a doctor is skyrocketing. It is easy to see that the average debt of medical students is a perfect indicator of this. In 2016, the AAMC found that almost 74% of medical students graduated with tuition debt. The median load turned out to be a whopping $190,000. That’s a dramatic increase since 2000, when the average debt was only $125,372. Get this, some student loan debt can climb up to $300,000. That hurts a bit even just to read.

Further reading: The Reality of Medical School Debt

So, how can we best prepare ourselves to be as cost-conscious as possible when tackling med school? Here are our tips:

Don’t Lose Hope

However staggering the numbers seem, don’t let them deter you from pursuing a true calling to medicine. You’re allowed to be conscious of (and maybe even a little stressed about) the amount of money you will need to spend on medical school. The general consensus, though, is that’s it’s worth the investment.

The job security and income potential attached to a medical career can make up for the enormous front-loaded costs. In fact, senior AAMC research analyst, Jay Youngclaus, confirmed in a 2013 study that physicians in all specialties could still pay back their medical school debt without incurring additional debt. Julie Fresne, the Director of AAMC Student Financial Services contends the same. “There is a concern that the cost of medical school will deter otherwise qualified and underrepresented candidates,” she worries. “We’ve got to get to people younger, earlier; we’ve got to help them understand that they can afford a career in medicine.”

You may not realize it, but there are numerous resources and opportunities available to you to cut the cost of your medical school education. Here are five tips to help you lessen the financial burden.

Senior AAMC research analyst, Jay Youngclaus, confirmed in a 2013 study that physicians in all specialties could still pay back their medical school debt without incurring additional debt.

1. Be Proactive

It’s never too early to start researching your financing options at your prospective medical schools. This should begin with some honest assessments. What level of financial support, if any, can your family feasibly provide? How much can you individually contribute from savings? Once these questions are sorted out, figure out how much tuition remains to be covered. Step two will help you address this remaining number.

A unique and financially more reasonable option to consider is attending a three-year MD program. Be prepared – the curricula of these programs will be substantially more rigorous; at the same time, successful matriculation will often guarantee a spot in a specialized residency.

Let’s say, for the sake of the majority, that you are planning on pursuing the typical 4 year medical school path.

2. Explore Student Financial Aid

Most of you may have explored financial aid options while applying to college. Remember those acronyms: FAFSA, CSS, and SAR? They’ll be relevant again when applying to medical school. Don’t hesitate to reach out to the financial aid officer at each of the schools to which you apply in order to gauge what your financial aid package may entail. These advisers know best what their institutions can offer you, as well as when the funds will be available to you. They can shed light on whether need-based and merit scholarships are offered, and whether full tuition coverage is a possibility.

While you’re doing this, however, know the lingo. Make sure you know the difference between grants (no repayment) and loans (must be repaid). There is also a difference between loans that you have to pay back with interest versus those that do not include interest. Large loans with a high interest rate are going to be exponentially more difficult to pay down, but are unfortunately the most common.

Educating yourself about all of the different ways you can take out loans, as well as knowing exactly how much you need, can help you from falling into the trap of accepting too much aid that will be a pain to repay later.

3. Pay when you can

Once you can factor in the school’s aid, do the math. Use online calculators and figure out what amount is left. Estimate important things like whether you’ll need to find a part-time job, and how much you would ideally need to make. This is for two important reasons: so that you can have money for other interests and so that you do not have to defer loans until residency. Pay what you can while in school, as it will help prevent your balance from exploding once the deferment ends. For instance, with a student balance of $164,800 and 6.00% rate, holding off student loans for residency can add about $30,000 in accrued interest. This would make your new balance about $194,000, and bump up your monthly payments to more than $2,000. Eventually the total cost (including interest) will be about $260,000 repaid over a decade. Make a goal to not pay back more money than you actually owe.

4. Get loan smart

Let’s back up a little bit. When you do choose to take out loans, it’s important to make decisions with the understanding that not all loans are created equal. Students often make the mistake of thinking that the loan with the lowest monthly payment is the best, but this is not always the case. Get as much information as you can regarding interest accrual, deferment options, add-on fees at repayment, and payment plans to make an informed decision. These are all factors that separate good deals from great ones and SimpleTuition can help you calculate all that. If federal student loans aren’t enough to cover the cost, private loans are another option to consider. However, these tend to have many caveats, such as more variable interest rates and non-tax-deductibility.

When you do choose to take out loans, it’s important to make decisions with the understanding that not all loans are created equal.

While finding the best loans, you can help set yourself up for the best loan arrangements by maintaining not only a strong credit score, but also a good credit history. This is especially important when seeking private loans, as the credit score and credit history together inform the private loan lenders whether they can entrust you with a loan. It is important that you have no open collection accounts, delinquent student loans, or “maxed” out credit cards. Make sure you’re in good standing by reviewing your account through your free annual credit report.

Another important thing to know is that you may not be able to take out a private loan by yourself. If you do not qualify to take a loan out by yourself, you will need to do so with a co-signer; often times this will be a parent or guardian, but can be a large financial liability for the co-signer as well. In the case of needing a co-signer, make sure that all parties are aware of the amount, interest rates, and risks involved should you not be able to pay the loan back in a timely manner.

5. Consider Repayment and Forgiveness Programs

If you are willing to commit to practicing medicine in underserved areas or serving as a military physician, there are numerous programs that will subsidize your tuition in exchange for promised work. These include, but are not limited to, the Indian Health Service Corps Scholarships, the Armed Forces Health Professions Scholarship Program, and the National Health Service Corps. There are also other loan forgiveness programs that cover a portion of debt in return for at least two years of service in underserved areas through the nation.

PSLF (Public Service Loan Forgiveness) is another option. We wrote an entire blog on this topic as well, as it is a bit more complicated. The bottom line is that PSLF offers tax-free forgiveness of student loans after ten years of qualifying payments. The caveat? Very few people have successfully received loan forgiveness under this program, and it is not expected to stick around as an option forever.

Conclusion

Medical student debt doesn’t have to be daunting. With research, planning and flexibility, you can cut down on your total out-of-pocket costs while managing your payments well. In addition to reflecting on the tips I’ve presented above, ask yourself some questions, like the following.

-

“Is a separate financial aid application required at my prospective school?”

-

“If I get a scholarship for a year, will I be guaranteed to receive it in the successive years?”

-

“How can I budget my money to cut down on my spending and borrowing?”

Pondering the answers and planning accordingly can help you make great strides when tackling your future medical school debt.

Now we have a question for you to answer below in the comments: would you consider getting a job while in medical school?

Our Alumni Enter Great Medical Schools

John Daines

- Atlantis '17

- Brigham Young University '19

- Washington U. in St. Louis MD '23

Zoey Petitt

- Atlantis '17

- U. of Arizona '18

- Duke MD '23

Zoey Petitt

Hungary ’17 || University of Arizona (undergraduate) ’18

Completed Atlantis Program Location and Date:

Hungary, Summer 2017

Do you believe your Atlantis experience helped you get into your graduate program?

I believe it was very helpful.

Generally, why do you think Atlantis helped you get into your graduate program?

For me, my Atlantis experience played a key role in confirming my decision to go into medicine. This was important for me to discuss during the admissions process.

Specifically, did you talk about Atlantis in your interviews?

Yes

Yong-hun Kim

- Atlantis '17

- Stanford '19

- Mayo Clinic MD '24

Yong-Hun Kim

Budapest, Hungary ’17 || Stanford University

Program:

Budapest, Hungary – Winter 2017

Undergraduate:

Stanford University class of 2019

Major:

Computer Science

Honors:

Bio-X Grant (award for research)

Undergraduate Activities:

President and Founder of Stanford Undergraduate Hospice and Palliative Care, Volunteer for Pacific Free Clinic, Research Assistant in Wernig Pathology Lab, President of Hong Kong Student Association, violin performance

Describe Atlantis in three words:

Eye-opening. Spontaneous. Exhilarating.

Why did you choose Atlantis?

I chose the Atlantis program because it combines opportunities to shadow physicians and travel abroad, both of which I had little prior exposure to.

What was your favorite experience as an Atlantis participant?

My favorite experience as an Atlantis participant came in the stories exchanged over meals or excursions and the breadth of conversation that reflected the diversity of backgrounds within our cohort and site managers.

What was the most meaningful aspect of your time shadowing?

I appreciated the chance to speak with physicians in Budapest and hear their personal motivations for pursuing medicine because it really helped better contextualize and validate my own interest in medicine. The physicians were also just really welcoming, relatable, and down-to-earth people.

How has Atlantis helped equip you for the future?

The Atlantis program has equipped me with a better understanding of what a career in medicine looks like, which I think is an invaluable gift considering the long road ahead of those who aspire to be a physician.

How has Atlantis equipped you for active leadership in the medical field?

The ability to interact and empathize with patients of diverse backgrounds and communities is a necessity to be a leader in the medical field. I think the Atlantis program, through my interactions with mentors and their patients, has helped me take my first steps toward attaining the cultural vocabulary and literacy required of a physician.

Megan Branson

- Atlantis '18

- U. of Montana '19

- U. of Washington MD '24

Sarah Emerick

- Atlantis '19

- Eckerd College '20

- Indiana U. MD '25

Snow Nwankwo

- Atlantis '19

- Catholic U. of America '21

- Georgetown U. MD '26

Tiffany Hu

- Atlantis '16

- U. of Maryland '17

- U. of Michigan MD '22

Tiffany Hu

Tereul, Spain ’16 || U Michigan Medical School

Program:

Teruel, Spain – Summer 2016

Undergraduate:

University of Maryland class of 2017

Admitted medical student at:

University of Michigan Medical School

Major:

Neurobiology

Honors:

Honors Integrated Life Sciences Program, Banneker/Key Scholarship

Extracurricular Activities:

American Medical Student Association Co-President & Advocacy Day Liaison, Alternative Breaks Experience Leader, Health Professions Advising Office Student Advisory Board, Biology Teach Assistant, Health Leads, Buddhist Tzu Chi Foundation, NIH Research Intern, Physicians for Social Responsibility Environment & Health Intern

Describe Atlantis in Three Words:

Educational. Eye-opening. Exhilarating.

Why did you choose Atlantis?

I wanted to expand my horizons and understand a culture of health different from the ones I am accustomed to. I had shadowed doctors in the United States and Taiwan prior to my Atlantis program experience, and being able to see first-hand the healthcare system in Spain allowed me to draw comparisons between the different complex healthcare systems.

What was your favorite experience as an Atlantis participant?

Bonding with the other participants and celebrating our time together along with the doctors we shadowed. We would discuss our interests, passions, and motivation for medicine, and it was an incredible experience to learn from and alongside them.

What was your experience with the doctors you were shadowing?

Because of the pre-established relationships with the hospitals in which we shadowed, all the doctors were very welcoming and accommodating. They were willing to translate for us and explain in detail all of their medical decisions. My doctors and I had wonderful conversations about the differences between life in Spain vs. the United States.

What was the most meaningful aspect of your time shadowing?

I was excited to scrub in on surgeries and watch as the doctor explained what he was doing throughout the operation. Before and after surgeries, as well as in my other rotations, I observed how the doctors reassured and communicated with their patients. I was able to glean insight into differences between the experience of health in Spain versus the United States through observation as well as conversations with the doctors.

How has Atlantis helped equip you for the future?

Besides the wealth of medical knowledge I gained from shadowing the doctors, I challenged myself to step outside of my cultural comfort zone and explore more than I thought I was capable of. Atlantis allowed me to make connections with people from all around the United States and abroad, and the friendships I gained helped me learn so much more than I would have on my own.

Lauren Cox

- Atlantis '18

- Louisiana Tech '20

- U. of Arkansas MD '24

Lauren Cox

Libson, Portugal ’18 || Louisiana Tech

Completed Atlantis Program Location(s):

Lisbon, Portugal

Year of most recent program:

Fall ’17 – Summer ’18

Season of most recent program:

Summer

Do you believe your Atlantis experience helped you get into your graduate program?

Extremely helpful

Generally, why do you think Atlantis helped you get into your graduate program?

It exposed me to shadowing that was hard to come by in the states. It also gave me a chance to see other systems of healthcare.

Specifically, did you talk about Atlantis in your interviews? If so, how much relative to other topics?

Yes – they wanted to know about my experience, and specifically how the healthcare I saw in another country compared to what I had seen in the USA.

Kayla Riegler

- Atlantis '18

- U. of Kentucky '20

- U. of Kentucky MD '24

About Atlantis

Atlantis is the leader in pre-health shadowing and clinical experience, offering short-term programs (1-10 weeks) over academic breaks for U.S. pre-health undergraduates. Medical schools want 3 things: (1)healthcare exposure, (2)GPA/MCAT, and (3)certain competencies. Atlantis gives you a great version of (1), frees you to focus on (2), and cultivates/shows (3) to medical school admissions committees.

Watch Video: The Atlantis Shadowing Experience and How it Helps In Your Med/PA Admissions Future

More Blog Posts

What Pre-Med Extracurriculars Are Ivy League Students Doing Right Now?: A LinkedIn Analysis

What Kind of Students Do Elite Medical Schools Actually Profile on Their Sites?

Two Atlantis alumni admitted to Top 5 MD programs wrote our widely read medical school admissions guidebook — download yours.

Get our 76-page medical school admissions guidebook, by Atlantis alumni at Harvard Medical School and Stanford School of Medicine.